The changes to the Tax Agent Services Act (TASA) aim to close regulatory gaps and include prohibitions around false and misleading statements. They also cover obligations for practitioners to disclose significant matters relating to clients such as tax offences or previous convictions.

De Cure said the reforms represent a nuanced approach to professional standards that recognises the differing scales of practices from small operators to the Big Four firms. The reforms will take effect from 1 January 2025 for larger practices with more than 100 employees, and 1 July 2025 for smaller practices.

TPB ‘not the Spanish Inquisition’

De Cure reinforced that the expectations of a small and medium practice were “entirely different to our expectations of a big four practice”. “I can also assure you that there will be no TPB investigators knocking on your door asking you to see your quality management system or asking to see your records of whether you’ve dobbed somebody in or asking you whether you have implemented one specific item in these new obligations,” he said.

While the TPB will investigate breaches carefully, de Cure insisted it will not be the “Spanish Inquisition”. “I think you’ll find that for those of you who are consistently doing the right thing, you are not going to see much,” he said.

De Cure commends IPA’s advocacy

The announcement to extend the deadline for small businesses for the changes to come into effect follows consultation with the professional bodies, including IPA, over concerns about whether there was sufficient time for businesses to meet the new compliance requirements.

De Cure congratulated IPA on its “mature and constructive” advocacy that had “been an important part of the debate”. “It’s been a really important part of the place that we’re in at the moment to get these new law changes into a slightly better place than perhaps they started,” he said.

He said his role is to “build a bridge between the organisation that’s the TPB and the tax profession”. “Having a level playing field is one of the things that protects you from unfair competition, and it protects you from clients who want to drag you down a road, potentially doing the wrong thing.”

Practitioners will have expanded obligations to keep clients informed. They must explain the existence of the TPB, how to access its register and the complaints process. Crucially, practitioners must disclose professional events from the past five years, including suspensions, bankruptcies, criminal conviction and significant legal penalties.

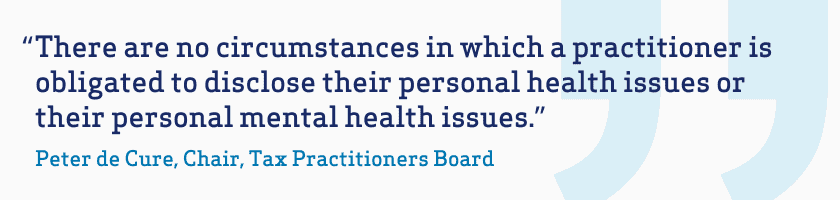

De Cure said the implementation would be practical and proportionate, alleviating concerns about disclosure requirements. “There are no circumstances in which a practitioner is obligated to disclose their personal health issues or their personal mental health issues,” he said. “It’s just not happening.”

False and misleading statements require immediate action

The new code introduces obligations for practitioners to take immediate action if they become aware of false or misleading statements from clients by correcting the record with the Australian Taxation Office (ATO) or the TPB. In circumstances where a client has made a false statement and refuses to correct it, practitioners are required to withdraw from the engagement and notify the TPB if the statement could cause substantial harm.

“You’ve got a client that you reasonably know has made a false or misleading statement,” he said. “We’re saying that’s not a suitable client for you to be involved with.”

Practitioners must also maintain comprehensive records of their tax services for five years and include key documentation such as engagement letters, fee notes and file notes demonstrating the basis of professional advice. De Cure warned practitioners using cloud services must ensure either full encryption or obtain written client permission.

Quality management systems must be implemented and reflect the practice’s size and scope. For sole practitioners, this might involve self-assessment, while larger firms will need more sophisticated approaches. Key elements include governance arrangements, performance monitoring, conflict of interest policies and robust recruitment and training protocols. De Cure stressed that cyber security should be a critical consideration, noting that tax practices are “data-rich environments for a cyber hacker”.

De Cure challenged practitioners to uphold the profession’s integrity, discouraging conduct that undermines public by maintaining constructive dialogue with professional bodies, the ATO and government agencies. He acknowledged the profession’s challenges, referencing the tax gap and instances of aberrant behaviour. However, he commended the majority of practitioners who do the right thing.

The TPB has already published six draft guidance documents following consultation with professional bodies. They will be finalised and released before Christmas to give practitioners comprehensive guidance.

Practical TASA tools for accountants

In a subsequent session, Arthur Athanasiou, partner at Thomson Geer, deconstructed the TASA reforms to help tax practitioners navigate the new regulatory regime. He said tax agents must now adhere to an expanded set of professional conduct requirements, with the number of code items increasing from 14 to 17.

Athanasiou said the TASA reforms were the most significant in recent times since the introduction of capital gains and fringe benefits taxes. “I really can’t remember such a change to the level of laws…that regulated the profession,” he said.

He said self-reporting significant breaches could include systemic minor errors that could trigger reporting requirements, Athanasiou said.

The new regulations introduce critical employment and engagement restrictions. Tax agents cannot employ or contract with disqualified entities without explicit TPB consent, including contractors and employees. A previously registered tax agent whose registration was terminated cannot simply transfer their client base through informal arrangements.

As compliance requirements become more complex, the value of professional tax services increases. Practitioners should consider whether their current fee structures adequately reflect the expanded professional responsibilities, Athanasiou said.

His practical recommendations include:

- Review all existing client engagement arrangements.

- Update employment contracts with disqualification clauses.

- Implement systematic breach identification processes.

- Develop clear protocols for handling potentially false statements.

- Create transparent communication mechanisms with clients about mutual obligations.

Athanasiou cautioned the new regulations require proactive, strategic approaches to professional practice to maintain high ethical standards, protect client interests and preserve public confidence in tax advisory services.

Want to learn more about the latest developments and issues affecting the accounting landscape which was discussed at the 2024 National Congress? Read the next article in the 2024 National Congress series: Member Awards winners announced