At a glance

- SME borrowing conditions are the most favourable they have been in several years.

- Banks and non-bank lenders are actively targeting the SME sector for business growth.

- Competition has improved pricing, application processes, and the range of available funding products.

- The positive outlook could be threatened if the Reserve Bank raises interest rates.

Small and medium enterprises (SMEs) looking to borrow are entering 2026 with the most favourable conditions in several years.

Even though many SMEs still face lending challenges, traditional banks and non-bank lenders alike are focusing on the sector as a source of growth.

This change in lenders’ attitudes has helped to push up indicators of small business optimism. The Australian Small Business and Family Enterprise Ombudsman (ASBFEO) Small Business Pulse publication reports “strong momentum amongst small businesses to explore growth and transformation”.

Small business is out of the pit

ASBFEO Small Business Pulse changes, quarterly

Note: Scale starts at 75. The ASBFEO Small Business Pulse did not reflect a COVID-related fall in 2020 as government support measures outweighed other economic impacts. As economic activity, including insolvencies, have returned to trend levels, the Pulse has reflected these shifts.

Source: Australian Small Business and Family Enterprise Ombudsman (ASBFEO), 2025.

And so long as the Reserve Bank of Australia (RBA) does not find reasons to start tightening interest rates again, lending conditions may even improve further during 2026.

The banks’ new attitude

The SME sector accounts for around half of total business credit in Australia. Aiming to gather the most recent signals from the sector, the RBA not only assembles formal statistics but also maintains a Small Business Finance Advisory Panel.

The borrowing signals from that panel have turned positive, says the RBA.

“Panellists and liaison contacts suggest that access to finance for SMEs has improved along numerous dimensions over the past couple of years”, RBA officials say in an article in its Bulletin in late 2025.

These dimensions include:

• more competitive pricing;

• faster approval times;

• more streamlined application processes; and

• a broader range of funding products – including improved availability of unsecured funding or funding that is not secured by physical assets such as property.

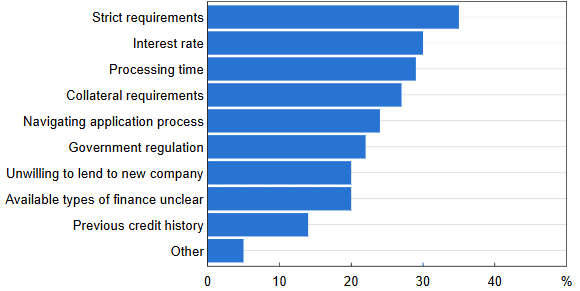

The RBA acknowledges that “for many years small businesses have reported challenges in obtaining finance”. Citing a Banjo Loans survey, it lists challenges such as strict lender requirements, high interest rates, long processing times and requirements to provide property or personal assets as collateral.

Borrowing still presents challenges

Share of SMEs who experience challenge*

* Note: Responses from those SMEs that experienced challenges when obtaining finance. Categories not mutually exclusive.

Source: Banjo Loans; RBA

But the RBA assessment and other signals suggest a clear turnabout from years of complaints by the SME sector over access to credit.

The major banks are keen to reinforce the RBA panel’s message.

“The industry is very eager to grow in small business. Actually, if I had to say it, the hottest part of the market, in terms of intention of the industry to grow, is in small business” Nuno Matos, the CEO of ANZ, told the Economics Committee of Parliament in mid November 2025.

“We have lots of appetite for lending to small and medium-sized businesses” NAB CEO Andrew Irvine said.

“That doesn’t mean that everything is perfect in terms of access to capital for small and medium-sized businesses.

“It’s true to say that Australia tends to focus on more secured lending than unsecured lending. Some of that is because secured lending is cheaper for the borrower and, therefore, it could be the customer’s wish to actually have security over a physical asset – because it means they can avail themselves of lower levels of interest.

“But it is still the case that, when you look at the mix of lending in our country, it does skew to secured versus unsecured.”

Westpac CEO Anthony Miller confirmed that like the ANZ, his bank is keen to increase its small business lending. “It’s a real area of focus for us,” he told the committee.

How the banks rethought SME lending

Miller explained one dimension of the bank’s approach to lending relevant to many borrowers – the banks’ assessment of cash flow.

“One of the areas that we have been very focused on is, if we are the transactional bank partner to the business – that is, they use us to hold their liquidity, receive payments, make payments et cetera – it means we are in a very privileged position to understanding their cash flow and the various impacts on their cash flow over time.

“That puts us in a very good position to be able to go and lend money to that customer.

“One of the initiatives we have had over the last couple of years is to look at all of the SME and small business customers that we have where they have their transactional bank account with us so we can understand their financial performance. We have been able to identify the amount of financing we can provide them.

“We’ve been able to predetermine that we have the appetite and the capacity to lend them a certain amount each, and we are engaging with all of them in making sure they understand that we have capacity and have appetite to support them.”

This means for many prospective borrowers, the most plausible lender they can consider is the bank they use for their transactional banking. In particular, small businesses should engage with the provider of their merchant acquiring facility – that is, the bank which receives their debit card and credit card payments.

Commonwealth Bank has been growing much faster in business lending than any other bank in recent years. In front of the committee, CEO Matthew Comyn explained how the bank has been improving its lending processes for small and medium business. “We are taking more risk in a number of areas,” he told the committee.

“During COVID, we originated more than half of the SME loan guarantee. We’ve turned that now into a $10 billion unsecured loan book.

“The process around that, to get funding and financing, is sub-15 minutes. We’ve expanded things like working capital.”

Competition for SME borrowing

This pivot to a stronger strategic focus on the SME sector has contributed to stronger competition in the business lending market, the RBA explains in its Bulletin article.

“Stronger competition has supported the supply of credit to small businesses, particularly over the past year, through more competitive pricing, improved application processes and an incremental easing in lending standards from some lenders.”

Outside of the big banks, many smaller lenders are volunteering to fulfil business demand for credit.

The competitors include lesser-known names like the new Judo Bank, a dedicated business lender, and Great Southern Bank, the former Credit Union Australia, which in the last year or so has made lending to small business a pillar of its strategy.

But beyond the banks lie a group of non-bank lenders that includes asset financiers (often tied to the firm whose assets they are financing) and an increasingly diverse range of private credit firms.

In recent years, specialised lenders and alternative forms of finance have gained market share within the SME lending market, the RBA said in its Bulletin article. That has increased the breadth of financing options available to smaller businesses

The non-bank share of SME lending has increased strongly since the start of 2022, particularly for smaller loans, the RBA says.

All of these lenders have been investing in technology to “reduce loan approval times, simplify application processes and improve access to banking services”.

And in a final sign of improved competition, the RBA says that broker activity in the SME market has also increased,

(The now much-discussed private credit sector is also becoming an increasingly important component of the non-bank lending segment. But typically private credit firms target larger businesses, rather than SMEs.)

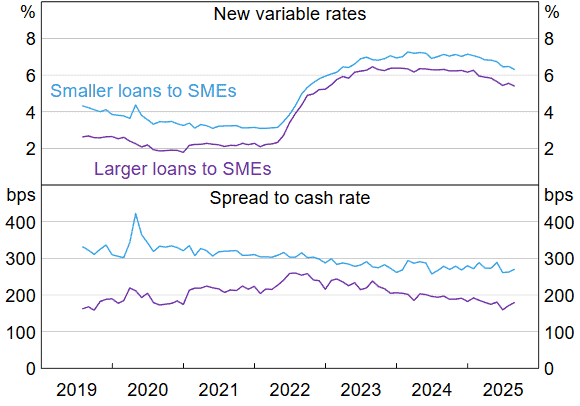

Falling rates

The interest rates small businesses pay on loans, on the face of it, are not that prohibitive, on average.

Indicator lending rates compiled by the RBA show that for a small business term loan the rate is around 8%.

For an overdraft this rate is around 10%.

Money.com.au, a service that compares business loans, lists the “best business loan rates” on products it compares at a significant margin over the RBA’s average.

But the RBA also says that borrowing costs have declined by a little more than the cash rate. And the spread between SME and large business lending rates has narrowed to a historically low level.

SME rates start to drop

Variable SME lending rates 2019-2025

Source: RBA

Finance that is unsecured or secured by non-physical assets has reportedly become more readily available, though unsecured credit remains a small share of overall small business finance.

“Several factors could explain why the share of unsecured small business credit has remained very low” the RBA said.

“It may be that unsecured finance has only become marginally more accessible, or that increased availability of unsecured finance has not been met with increased demand.

“Consistent with the experience reported by panellists, customers may also be more likely to take out these loans for only relatively short timeframes (e.g. to manage temporary cash flow issues) given these loans are typically extended at higher interest rates.

“Furthermore, some non-bank providers of unsecured lending are not well captured in official data sources.”

Applying for a loan

The process for applying for business loans is, by and large, getting easier.

“Many lenders have invested in digitisation and automation over the past few years to improve processing times, simplify application processes and reduce costs” the RBA analysis says.

“This includes making use of customers’ transaction histories and bank statement analysis to automate loan decision-making.

“Numerous lenders have also simplified the loan application process by relaxing their documentation requirements for smaller SME loans.”

Rate rises remain an enemy

As the RBA points out, small business is hardly in boom times. Economic conditions for the sector have improved since 2024, but the RBA says they “remain subdued” – and weaker than for large businesses. Cost growth has eased, but cost pressures remain “elevated by historical standards”.

And just as the sector’s borrowing recovery was sparked by interest rate falls, a new round of interest rate rises could conceivably cut it short. Indeed, Banjo Loans warned in January 2026 that just the suggestion of new rate rises has cooled demand for lending among larger SMEs.

Small business borrowing is much easier than it was in 2023. Lenders are more open to negotiating. But the sensitivity to interest rates seems as strong as ever.

Explore the IPA’s online CPDs to enhance your skills, from self-managed superannuation funds to tax updates.