At a glance

- The Productivity Commission sees SMEs as key to Australia’s economic revival.

- It proposes a 20% tax rate below $1bn revenue and a 5% cashflow tax.

- The goal is to reverse falling business investment and boost national productivity.

- Proposals face criticism over complexity, risks, and unconvincing regulatory plans.

The Productivity Commission’s new report on economic dynamism shows it turning towards the small and medium business sector as a source of economic revival.

The Commission’s August 2025 interim report focuses on two issues which the IPA and other small business voices have long seen as priorities: lower SME taxes, and reductions in the regulatory burden.

Most observers are sceptical about the latest in a long line of suggested crackdowns on regulation.

But the Commission’s suggested 20% tax rate on companies with revenue below $1 billion has sparked interest. And it has combined that cut unexpectedly with a new, universal 5% net cashflow tax.

A change in tax goals

For decades, governments have seen the nation’s biggest businesses as the nation’s best chance at creating vigorous industries. The tax system reflected that: governments might sympathise with smaller businesses, but they couldn’t see a compelling case for giving them an advantage against the giants who they thought of as Australia’s corporate champions.

“Implementing a cashflow tax for the very first time… is a high risk business.”

Vicki Stylianou

But that started to change in the 2010s, when first Julia Gillard’s government proposed a lower rate for smaller businesses, and then Malcom Turnbull’s government legislated it. Australia’s two-tier company income tax rate now stands at 25% for companies with turnover up to $50 million, and 30% for companies with higher turnover.

The Commission’s latest suggestions take that approach and amplify it. This two-tier approach is something that independent economist Nick Gruen, himself a former Productivity Commissioner, says “would have been anathema to the [Commission] of 15 years ago”.

Fixing business investment

As Public Accountant has noted, SMEs consistently underperform their larger counterparts on the one metric that matters most: productivity. So improving SME productivity is one of the most promising ways to boost Australia’s economic growth.

Productivity is the ultimate economic magic trick: it lets us achieve more with no extra effort. Today’s farmers, for instance, toil no more than the farmers of 200 years ago, but they use huge harvesters and tiny drones to do the same work for which their predecessors employed 100 labourers. That sort of productivity boost, repeated across the country in all sorts of industries, gives the average Australian a vastly higher standard of living than we had in 1825.

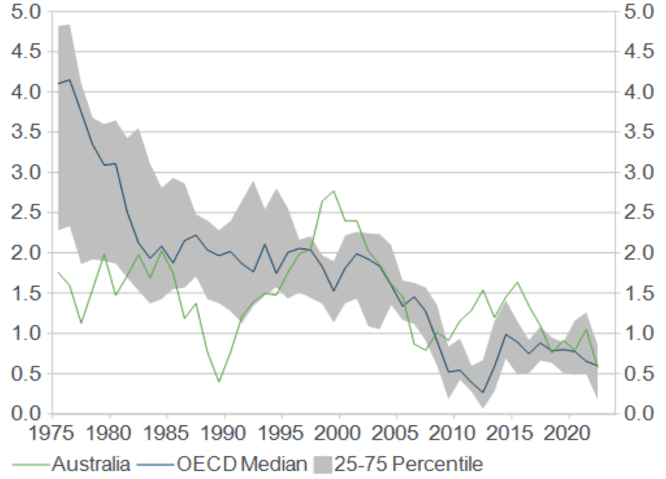

Yet like most OECD economies, Australia has suffered a sharp fall in measured productivity growth since the year 2000 (see chart). Australia’s productivity fall steepened noticeably after the mining boom petered out in 2015.

Australia’s long productivity slide

Rates of productivity growth in Australia and other OECD economies, percent, 1975-2023

The Commission has diagnosed this Australian productivity slide as largely a result of falling business investment. By recommending both a cut in profits tax and a new cashflow tax, the Commission hopes to give businesses enough incentive to start investing more intensively again.

The surprise is that the Commission has specifically targeted businesses other than the nation’s corporate giants. It says it has evidence that smaller firms respond better to company tax cuts. It argues a lower tax rate should lead to higher retained earnings and capital expenditure. And it says specifically that “this channel is particularly important for companies that do not rely on overseas markets for capital” – a group that is mostly small and medium businesses.

As our examples in an accompanying story show, the Commission’s tax changes would likely boost the after-tax profits of high-investment businesses. These businesses might be small builders or manufacturers, or giant miners, but if they invest their cash, they would likely gain from the Commission’s tax package.

By contrast, the big losers from the package seem likely to be giant companies – think of retailing giants – earning a steady living without huge investment. An example might well be a large retailer.

The devil in the detail

The detailed criticisms of the Commission’s proposed tax package have not yet come into focus. But they are likely to be many.

IPA Group Executive for Advocacy and Professional Standards Vicki Stylianou argues that the government still needs to address personal income tax and the GST, in particular, as well as the full range of federal and state taxes on everything from property to payroll.

IPA General Manager of Advocacy and Emerging Policy Michael Davison pinpoints the complexity that a new tax will bring for smaller businesses. “It’s another tax you will have to keep track of”, he says.

And there are other potential challenges.

- Implementing a cashflow tax for the very first time in a major economy is a high-risk business, Vicki Stylianou warns.

- If implemented, its effects will be impossible to show in economic models; many issues may only emerge once it is implemented.

- As IPA General Manager of Technical Policy Tony Greco points out, many of the broad strokes of the proposed cashflow tax still need to be filled in – such as how “cash” is to be defined.

- Davison notes that while Australia clearly needs more investment in human capital, this does nothing to encourage it.

- The proposed changes do nothing for many large businesses (the Business Council of Australia has already signalled its opposition).

- The Commission says it has not decided how its proposed system would interact with Australia’s longstanding dividend imputation system. Yet, as Nick Gruen observes, the costs involved here might determine whether the proposal is revenue-neutral, as the government is asking for it to be.

- It’s not clear that tax reform and a new call to lift the regulatory burden will be enough to kick-start Australian productivity. Other issues – such as technology adoption rates and access to finance – are also regularly suggested as crucial parts of any solution.

What’s changed on regulation?

The second part of the Commission’s prescription is a war on red tape. The report argues that “excessive or inappropriate regulation” is shackling businesses and stifling innovation and competition. Most IPA members would likely agree.

But the Commission’s report lacks any convincing ideas on why the war will go differently this time. Most observers are unimpressed by ideas such as the Commission’s call for “a whole-of-government statement to commit to regulation outcomes that better promote growth and dynamism”.

Stylianou says she has been hearing such calls “for more than 20 years. What’s changed?”. The government continues adding new regulations even as it talks of smarter and more streamlined regulation, she notes.

Davison says the previous government established an entire “red tape task force” in the Department of Prime Minister and Cabinet – but it made little impact.

Economist Nicholas Gruen of Lateral Economics is equally blunt: if a body suggesting a regulatory crackdown can’t explain why all the previous crackdown suggestions have failed, he says, then “it’s not putting itself in play to be part of the solution”.

Starting a discussion

The Commission’s final report is due in December 2025. Between now and then it will need to refine its modelling, and try to come up with a more impressive plan for tackling the regulatory burden.

But it does at least stand a chance of setting up a more fruitful tax discussion than Australia has had in recent years. That part of the Commission’s work, says Davison, “needs to be applauded, because they’re putting something different out there”.