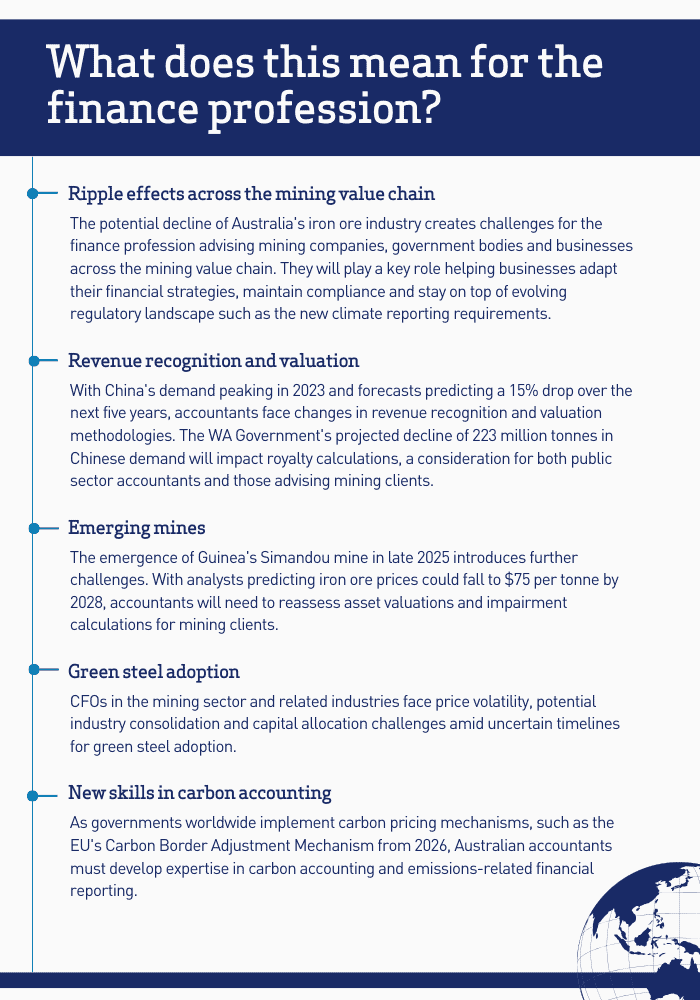

At a glance

- China’s demand for iron ore to make steel has fuelled Australia’s rise in wealth over the past two decades.

- Despite China reaching peak demand for iron ore in 2023 and a huge African mine coming online in 2025, Australia’s market dominance should remain intact for the medium term.

- A 25% tariff on all US steel and aluminium imports will test Australia’s dominance unless exemptions are secured.

- Green steel could disrupt this dominance in the long term; however, the technology is still uncertain, and the market needs government intervention to make it economical.

It is staggering to grasp the scale of Australia’s iron ore industry.

Since 2005, the iron ore industry has delivered Australia $1.2 trillion in revenue. Export income has risen from $8 billion a year to over $130 billion, and the volume of iron ore shipped from 230 million tonnes to around 900 million tonnes. In Western Australia, where almost all of the country’s iron ore is dug out of the ground in the Pilbara region, royalties from iron ore miners have accelerated from $1 billion to $9 billion.

Add in taxes paid by miners to the Federal Government and it is fair to say the iron ore industry has fuelled Australia’s meteoric rise in wealth over the past two decades. And it’s all thanks to China. China has had an incredible thirst for iron ore the last 20 years to make steel to build its rapidly developing economy. In 2023, it bought 85 per cent of Western Australia’s iron ore exports. The result has been an unprecedented golden era for Australian miners and the economy that is unlikely to be seen again.

“Although economic stimulus measures may provide short term support, the long-term outlook indicates a continued decline in demand in iron ore.”

Flavio Menezes, Director of the Australian Institute for Business and Economics at the University of Queensland

But with China’s economy now sputtering, with added pressure from Trump’s 10% additional tariffs on its imports, demand for the rock is starting to wane. African iron ore is about to flood the market, and green steel is an industry disrupter set to unseat Australia’s dominance. Things can only go downhill from here, but by how much?

A steady decline in demand

China’s slowing economy and the fact its steel mills have produced a surplus of steel has the WA Government marking 2023 as peak iron ore demand for China. It was up 3 per cent last year, but for the next five years, the WA Government is forecasting a 15 per cent drop in demand, equal to 223 million tonnes.

Flavio Menezes, Director of the Australian Institute for Business and Economics at the University of Queensland, believes this forecast is likely, irrespective of Chinese Government attempts to stimulate the economy.

“Although economic stimulus measures may provide short term support, the long-term outlook indicates a continued decline in demand in iron ore,” Menezes says.

“This was expected to happen, as the demand for steel falls as economies become more developed. For me, the only question is: how fast will demand fall?”

A drop in demand from China is expected to be buffeted by demand from other developing nations. According to WA Government forecasts, it won’t be enough. It expects Asian countries (excluding Japan, South Korea and Taiwan) to demand 66 million tonnes more in the five years to 2028, 157 million tonnes short of the fall in Chinese demand. A steady decline in global demand is the net result.

David Uren, Senior Fellow at the Australian Strategic Policy Institute, is upbeat about the prospect of Asian countries taking over the helm from China in their need for iron ore and steel.

“Vietnam, South Korea, India, Malaysia, Indonesia – these are all substantial emerging economies with a need to strengthen their urban and intra-city infrastructure,” Uren says.

“Steel is the essential skeleton of urban development. I don’t think we’ve seen the end of urban development across the emerging world by any stretch. Australia is well placed to supply rising steel production across the Asia-Pacific region.”

Africa’s coming of age

The flip side of demand concerns for Australian iron ore is the increase in global supply coming out of Africa, specifically the Simandou mine in Guinea. Once hailed as the ‘Pilbara killer,’ the Simandou mine has one of the largest and highest quality iron ore deposits in the world. It is expected to produce 2.8 billion tonnes over a 26-year lifespan, with production commencing late 2025.

Until recently, Simandou has been plagued by scandals and beset by infrastructure challenges. Dr Jeffrey Wilson, Director of Research and Economics at the Australian Industry Group, says the mine does not make economic sense, but China wants it to happen so it can reduce its reliance on iron ore from the world’s two largest producers, Australian and Brazil.

“At Simandou, they have to transport the iron ore 650 kilometres over pretty rough terrain with no other infrastructure in place. Also, it’s a long ship coming around the horn of Africa to China, which at periods of high oil mean high shipping costs. In my view, it’s a high-risk venture that’s going to be a sub-tier asset,” Dr Wilson says.

“It’s an expensive insurance policy for China, but for them it makes political and market structure sense.”

By the time Simandou ramps up production, some analysts are predicting the iron ore price – which is currently above $100 a tonne – will drop to $75 by 2028. With $40 the average cost of goods sold for Australian miners, Dr Wilson believes the extent to which Simandou can harm Australian miners depends on China’s appetite and how much they are willing to spend.

“It takes a long time to bring new iron ore capacity online. Most of the skill and technology is in transport logistics and getting the iron ore to port and onto a ship. Australia has figured that out before any other country, and to this day, does it at the lowest cost and in a high wage economy,” he says.

“The question is: how much is the Chinese system willing to funnel towards Simandou and other projects to get them to market? Because it will cost a lot of money, and there’s a lot of risk involved.”

“I don’t think we’ve seen the end of urban development across the emerging world by any stretch. Australia is well placed to supply rising steel production across the Asia-Pacific region.”

David Uren, Senior Fellow at the Australian Strategic Policy Institute

Like many in the market, Uren sees plenty of potential for African iron ore production but says efforts have gone nowhere in the last 20 years. Even with Simandou online, he says China will continue to buy iron ore from Australia because it has no other option for the “distant future.”

In the long term, Menezes believes Simandou is a big enough threat to Australia’s market dominance, and that Australia should be pivoting its strategy in preparation.

“In the near term, Australia remains well-positioned, but long-term uncertainties highlight the need for serious investment in green steel production,” he says.

Early days for green steel

For hundreds of years, steel has been made by using coking coal in a blast furnace to strip oxygen from the iron ore. Almost two tonnes of carbon dioxide are emitted for every tonne of steel, which has become a recent problem because of emissions targets. The steel industry contributes 8 per cent of global emissions.

Instead of using coking coal, green steel uses renewable energy or hydrogen. Globally, there are 37 active green steel projects, which sounds like a lot but many of the projects are in pilot stages. The technology is still uncertain and, most importantly, green steel is expensive to make compared to the blast furnace and coal method, which is why Uren says green steel is a slow burn.

“Hydrogen doesn’t burn as hot as coal. You’ve got to find ways of raising the temperature. From my understanding, the technology is still in development,” he says.

“Blast furnaces have got an average life of about 50 years. A lot have been built in China over the last decade, so blast furnace steel still has a long future.”

Governments a potential game changer for green steel

The game changer for green steel is government intervention. As governments respond to demands to reduce emissions to meet 2050 net zero goals, the steel industry could easily come into their crosshairs.

One legislative frontrunner is the European Union’s Carbon Border Adjustment Mechanism. Coming into full effect from 2026, CBAM is a tax on carbon to encourage cleaner industrial production. Dr Wilson expects it will create a price incentive to produce low emission steel.

“If you accept the premise that the net zero transition is going to happen in the world, we are going to have to have decarbonised steel. The fact that steel is in everything means there’s going to be huge rewards and gains for those who get there first,” he says.

“It’s when governments follow the EU’s lead and create a serious price wedge for green steel that the market for green steel will happen. That could be 2026 or it could be 2050.”

Australia, despite its abundance of iron ore and renewable energy resources, is not taking any giant leaps. The 2024-25 Federal budget allocated $18 million over six years to green metals initiatives. Dr Wilson says you need to add at least two zeros to that figure for it to have any real impact. In the commercial space, Rio Tinto, BlueScope and BHP have only recently dipped their toes with design and pilot studies.

The problem is green steel is not as simple as combining rocks with sunshine, says Dr Wilson. There is a complex global steel market to navigate in which Australia is not a major player. Also, governments will only fund the advancement of green steel technology if they can reap company taxes from onshore companies in return.

“What can Australia do to convince major global players to make green steel in Australia and not back in their countries? We have this issue in other industries, like the auto industry,” says Dr Wilson.

“Why would the Japanese Government spend billions of dollars creating competitive green steel technology only to build it in the Pilbara? The extent to which we get more of the action is going to come down to how we can be part of global value chains that are run and managed out of Tokyo, Seoul, Washington and Brussels.”

A lack of carbon pricing in Australia and the gradual decline of its steel industry does not give Uren much confidence about Australia’s prospects in green steel.

“In the last 15 years, there’s been a reduction in Australia’s production of metals. There’s a lot of steel grades we’ve stopped making. That’s all happening because Australia just can’t compete with China in terms of scale of operation and energy prices,” he says.

“As the industry diminishes, the pool of skilled engineers and geologists also diminishes. I don’t think we have the basic pool of expertise to be serious players in green steel.”

With the pathway to green steel production in Australia looking unlikely, the country appears to be prepared to ride out the iron ore tide.

The IPA is holding an event, Sustainability Standards – Global and Australian perspectives,

on 19 February about the latest International Sustainability Standards with Mark Babington, board member of the International Ethics Standards Board for Accountants (IESBA) and Executive Director of Regulatory Standards at the Financial Reporting Council (UK), and Channa Wijesinghe, Vice Chair of the IESBA and CEO, Accounting Professional & Ethical Standards Board. More information here.