Australia is moving towards a cashless economy, with digital transactions vastly dominating payments. This change presents both opportunities and challenges for small businesses, with questions emerging about a future without cash.

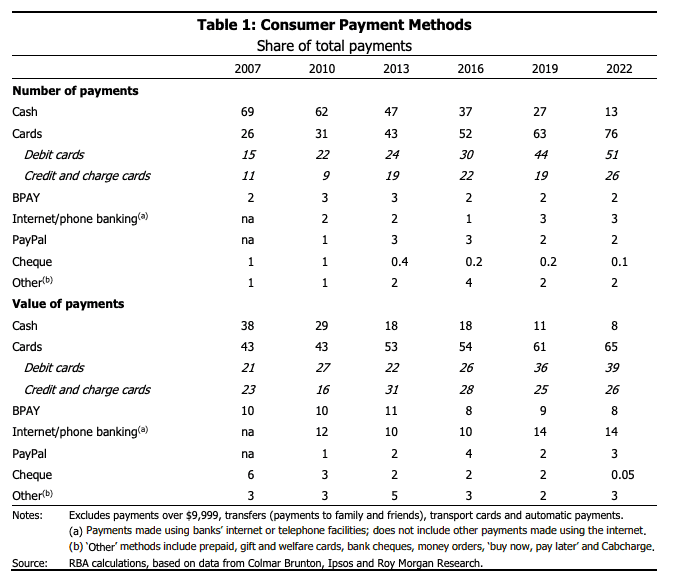

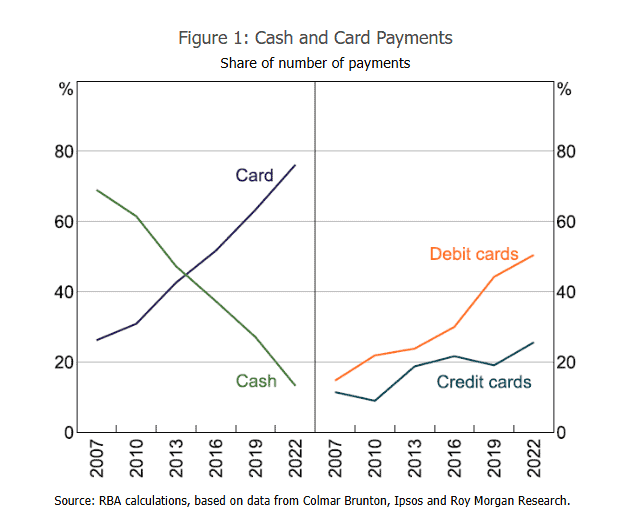

The pace of change has been rapid. As recently as 2007, 69 per cent of consumer payments were in cash, dropping to 27 per cent by 2019, and just 13 per cent by 2022, according to the RBA.

The COVID-19 pandemic accelerated the shift, when we turned to online payments from the safety of our homes and avoided handling notes and coins that we considered dirty.

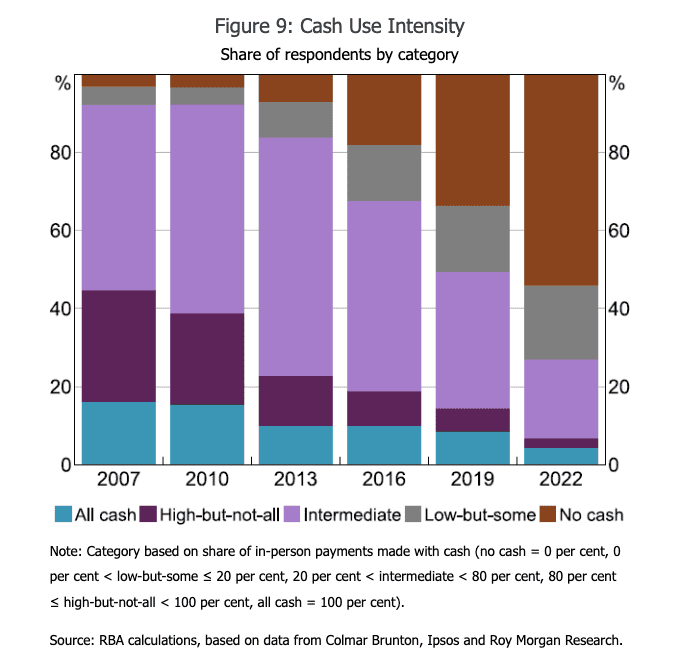

By 2022, over half of Australians used no cash in a week, up from about one-third in 2019 and around one-fifth in 2016.

Meanwhile, 75 per cent of consumer payments were made with debit and credit cards, up from 63 per cent in 2019 — alongside a steep rise in contactless and online payments.

Today, bank branches are closing, Osko enables instant transfers, BPAY bill payments are booming and we use cash-free businesses like Airbnb and Uber without a second thought.

Reserve Bank of Australia Governor Michele Bullock suggests cash might only last another decade, with its decline seen as inevitable. “Cash is not making a rebound. It is on a long-term decline because people find making electronic payments much more efficient,” she told a parliamentary hearing in January.

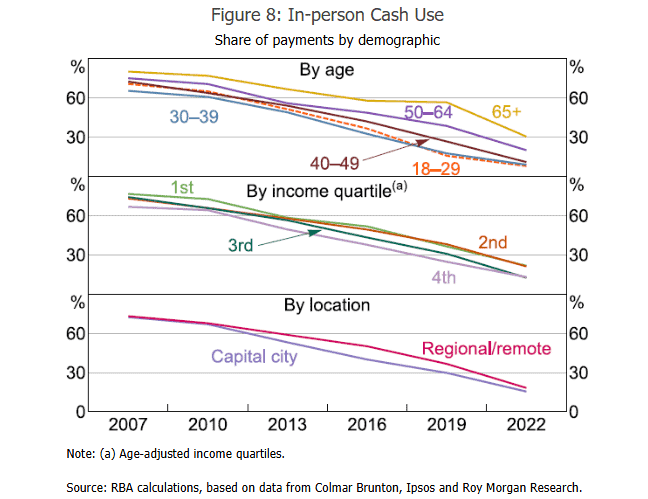

“We have the technology in place and we’re using it overwhelmingly — and we’re seeing this decline in the use of cash in all demographic groups and regions,” says Australian economist, journalist and commentator Peter Martin. “There’s nothing to slow down the cash transition.”

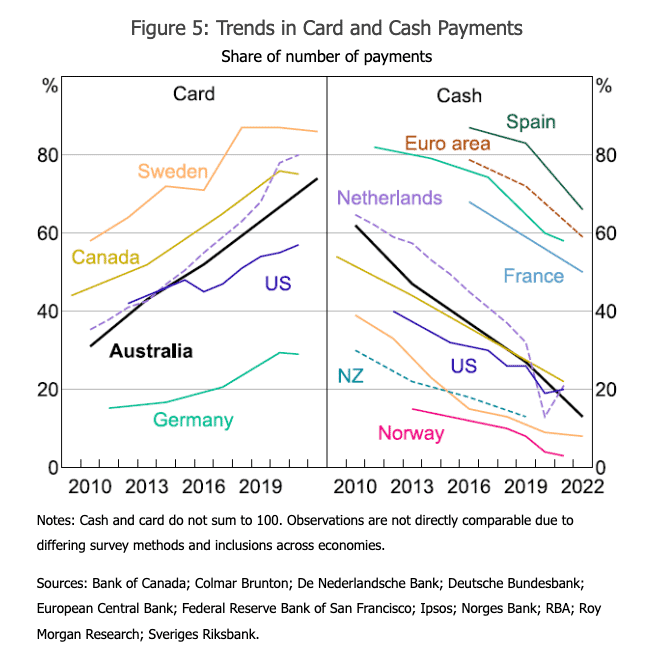

While the move away from cash is a global trend, the pace varies by country.

Norway, Sweden and New Zealand are seeing faster declines than Australia, whereas the US, France and the Netherlands lag behind.

In the Asia-Pacific region, Australia, China, Hong Kong, India, Japan, Korea and Singapore are leading the charge in digital payments, according to the United Nations Economic and Social Commission for Asia and the Pacific.

The benefits of going cashless

Experts agree that going cashless offers convenience and transparency, benefiting businesses through market expansion and improved efficiencies.

IPS says digital accounting platforms enhance transparency, tax compliance and counter the black economy.

“If everything is input into a reliable software system at the point of sale and there’s no need for manual cash counting or cash reconciliation, this simplifies and automates tax reporting, reducing errors and ATO penalties,” says Letty Chen, a tax advisor at IPA.

Digital transactions also aid the ATO in data matching, she adds.

“The ATO has agreements with banks and financial institutions to receive regular data, so if customers pay by card, this will clearly reflect in ATO records.”

A digital trail makes it harder for businesses to dodge tax responsibilities, says Martin.

“If a business favoured cash to avoid reporting to the tax office, or to under-report income for tax reduction or pension claims, they’re going to be increasingly out of luck.”

The risks of going cashless

The shift to a digital economy raises concerns about financial exclusion, privacy and security that need addressing, says Chen.

“People worry about scams and data access when making large payments online. Many times now, we’ve seen hackers get hold of customer data at large companies.”

System reliability is also an issue.

“Disruptions like software failures, internet outages or natural disasters complicate the move away from cash.”

Chen adds that some people rely on cash and might be disproportionately affected — especially those in remote areas with poor internet services, refugees or recent migrants, the elderly, people with disabilities, or victims of financial abuse.

“The government must invest in digital literacy and make digital payment services inclusive and accessible for everyone.”

Helping businesses in the cashless transition

Martin suggests that accountants can encourage digital adoption by charging more for handling cash. “With access to a digital accounting system, auditing takes a lot less time,” he says.

Chen says that accountants can guide clients in choosing the right software and leveraging available resources to organise and secure their digital payment systems.

She adds that businesses have a responsibility to enhance their own cybersecurity.

“With increased reliance on digital payments, staying informed about cybersecurity and industry-specific scams is crucial. Businesses should also have contingency plans in place for outages, scams or natural disasters so they can still access their payment systems.”

The Australian Cyber Security Centre (ACSC) offers guides for small businesses to protect against common threats, recommending multi-factor authentication, software updates and secure backups.

IPA also offers training delivered by Macquarie University Cyber Skills Academy to help accountants gain essential cyber security skills.

Payment regulations addressing new digital payment risks are essential to ensure the safety of funds and personal data.

The federal government is updating the Payment Systems (Regulation) Act 1998 to safeguard consumers by ensuring new systems like digital wallets (including Apple Pay and Google Pay) are regulated similarly to traditional credit and debit cards.

Meanwhile, the Scams Prevention Framework Bill 2025 sets up robust protections against scams, and new obligations for certain businesses in sectors targeted by scammers.

“At IPA, we’re keeping abreast of new laws and regulatory developments,” Chen says.

Ensuring cash for the short term

While Australia may be cashless in a decade, Bullock acknowledges the need to ensure cash accessibility in the short term. This is not as easy as it sounds; transporting cash around Australia is expensive for banks, which pass these costs onto businesses.

“As we use less and less cash, the cost of supplying it across Australia becomes prohibitive for banks and businesses, which is why they encourage card usage,” says Martin.

To maintain cash access, the Australian government plans to mandate that businesses selling essential services and goods with a turnover of at least $10 million accept cash payments, starting January 1, 2026.

“This ensures access to essentials like groceries and healthcare,” says Chen.

IPA has responded to the proposed mandate, suggesting refinement of the essential goods and services list, and proposing that the small business exemption turnover test be based on the most recent tax return to ease the regulatory burden — among other points.

Apps, cryptocurrencies — what comes after cash?

“The future is clear; cash is disappearing. The questions are how long will it take and what will replace it?” asks Martin.

He describes cards as an “interim” solution due to high fees, which impact debit cards as well as credit cards — despite the “minimal cost of moving money between banks”.

Martin suggests payment apps would be a cheaper alternative.

He points to the example of Chemist Warehouse, which is introducing QR code payments, or ‘Pay by Bank’, allowing customers to scan a code at checkout and make direct payments from their bank accounts, bypassing card fees.

As for cryptocurrencies, though some support them, Bullock says the RBA is focused on researching Central Bank Digital Currency (CBDC) as a potential complement to existing money. CBDC would be a digital form of Australia’s fiat currency, issued by the central bank.

There’s still a lot of research to be done, mainly to ensure people and businesses feel comfortable, says Martin.

“The challenge for the future is designing a payment system that guarantees absolute privacy, and we’re not there yet.”