At a glance

- The Big Four’s growth has slowed since 2018.

- A wave of scandals has eroded government trust and increased media scrutiny.

- Internal conflicts and a rigid partnership structure have blocked major structural reforms.

- AI threatens their business model and requires capital they may struggle to raise.

Prelude: Puzzling at the Big Four’s endurance

Back in 2018, University of Melbourne accounting professor Ian Gow and historian–author Stuart Kells published the first comprehensive history of global accounting’s Big Four – Deloitte, PwC, EY and KPMG.

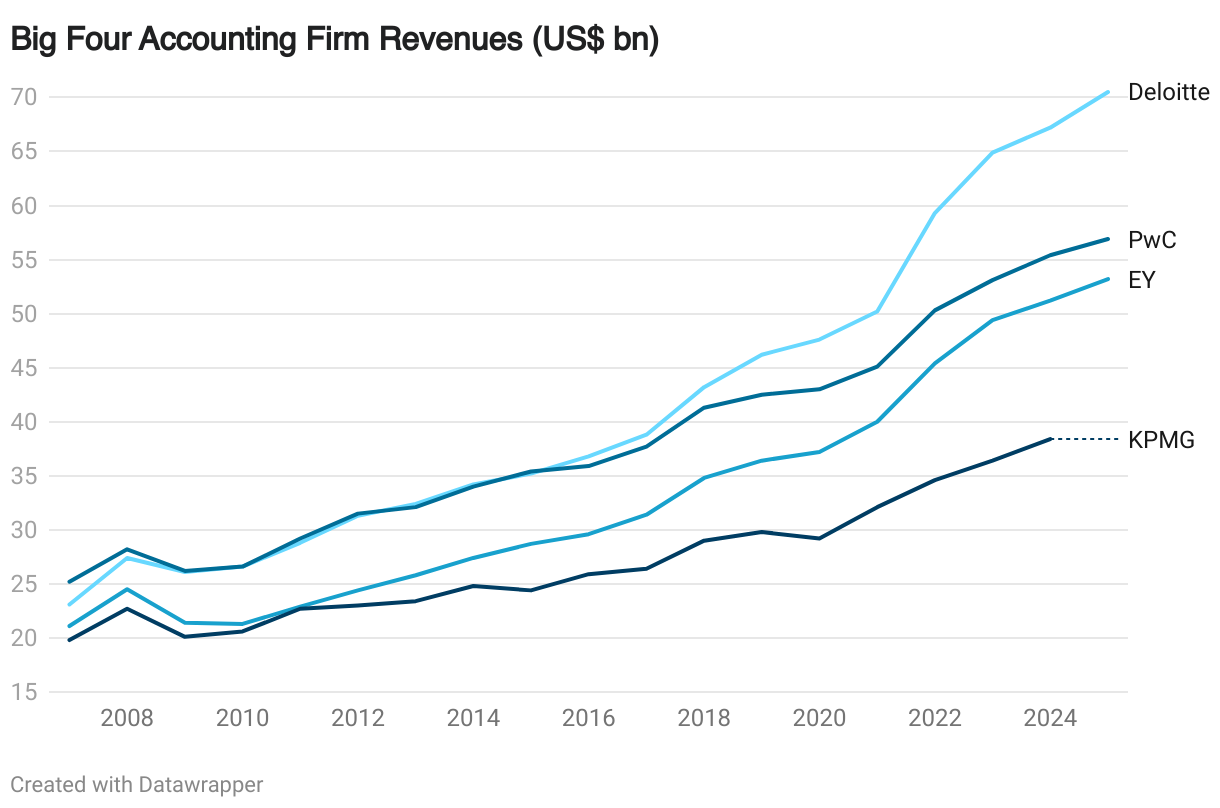

That book – The Big Four: The Curious Past and Perilous Future of the Global Accounting Monopoly – explained how its subjects had quietly grown. From unassuming 19th-century London origins, they had become 21st-century business powers with combined 2018 revenue of $130 billion. They were growing at 10% a year.

But in exploring the Big Four’s position, the authors admitted a certain puzzlement. The four firms had resisted scandals, internal conflicts and regulatory threats extending all the way to talk of break-ups. How had they survived? Would that resilience continue?

Seven years on, the Big Four have continued to grow. In 2025, their joint revenue reached US$219 billion (KPMG is yet to report). They employ around 1.5 million people.

But the growth has slowed and the questions remain. And the Big Four no longer look quite as resilient.

In tracing their recent fortunes, Public Accountant has turned again to one of the people who wrote the book on them, Ian Gow. He remains both impressed and a little puzzled by their continued dominance.

The Big Four face many threats

Gow and Kells’s 2018 book listed the many possible sources of trouble – threats from business rivals, government regulation, technology, misjudgement of risk, and contradictions within their business model.

Source: Big Four annual reports/Wikipedia

That proved a good call. There’s no denying the Big Four’s traditional tax and audit activities have kept on delivering revenue growth in the 2020s. But consulting and advisory revenue may, at least temporarily, have hit some sort of limit.

Source: Big Four annual reports/Wikipedia

And new hiring for the consulting businesses appears to have overshot, so that since 2023 the Four have pulled back, apparently aiming to reverse the fall in revenue per employee.

Source: Big Four annual reports/Wikipedia

Big Four scandals keep building

Seven years after writing his book, Ian Gow remains impressed at the Big Four’s ability to “manage their way through these scandals without being taken down by any of them”.

But Gow also points out the seriousness of many of the 2020s breaches. In the German Wirecard scandal, for instance, auditor EY somehow overlooked the fact that important elements of Wirecard’s business simply did not exist. “Wirecard was just off the charts,” he says.

And the sheer number of recent scandals is impressive. The Economist magazine estimated in late 2024 that the Four had paid four multi-million-dollar regulatory penalties in the years 2014-2019. But in the five years after that, it reported, they paid out a striking 28 multi-million-dollar regulatory penalties. One knock-on effect: the mainstream media, which once largely ignored the Big Four, now scrutinises them vigorously.

The following table summarises the most significant financial penalties and settlements identified by Public Accountant from 2019 to 2025.

Table: The Big Four’s 13 top scandals

| Firm | Incident | Jurisdiction | Penalty | Finalised |

|---|---|---|---|---|

| KPMG | Exam cheating | USA (SEC) | $US50m | 2019 |

| Deloitte | Autonomy audit | UK | $US19m | 2020 |

| Deloitte | 1MDB audit | Malaysia | $US80m | 2021 |

| EY | Exam cheating & obstruction | USA (SEC) | $US100m | 2022 |

| PwC | Tax leak & Scyne divestment | Australia | Est. $US450m revenue loss | 2023 |

| KPMG | Carillion audit | UK (FRC) | $US26m | 2023 |

| EY | Wirecard audit | Germany | €500k fine; 2-year ban | 2023 |

| Deloitte | China Huarong audit | China | $US31m | 2023 |

| KPMG | Exam cheating | Netherlands (PCAOB) | $US25m | 2024 |

| PwC | Evergrande audit | China | $US61.2m | 2024 |

| Deloitte | Backdating papers | Canada (Ontario) | $US1.59m | 2024 |

| PwC/Deloitte/EY | Exam cheating | Netherlands | $US8.5m | 2025 |

| Deloitte | AI errors | Australia | $US65,000 to date | 2025 |

Source: Public Accountant research

Governments losing faith?

For years, public-sector observers have asked whether outside consultants can really be relied upon to work in the public interest. The danger for the Big Four is that they now have credible case studies to support their doubts.

The past three years have seen two government-sector scandals emerge in Australia. This is a market where the Big Four have taken a notable chunk of what was once core government work. These two scandals (shaded in the table above) seem to be eroding that business, as centre-left federal and state governments take some of it back into government.

This appears to be one reason behind the end of the Big Four’s long run of Australian revenue growth. In 2025, each of the Big Four saw Australian revenue shrink.

Table: How the Big Four were slowed in Australia

Australian firms by revenue, $m, financial year 2025

| Rank | Firm | Revenue | Yearly change |

|---|---|---|---|

| 1 | Deloitte | $2,545m | -8.3% |

| 2 | EY | $2,430m | -2.7% |

| 3 | KPMG | $2,131m | -4.0% |

| 4 | PwC | $2,071m | -5.9% |

| 5 | BDO | $606m | +12.3% |

| 6 | Findex | $495m | +6.7% |

| 7 | RSM | $414m | +11.0% |

| 8 | Grant Thornton | $384m | +6.9% |

| 9 | Pitcher Partners | $356m | +2.0% |

| 10 | William Buck | $196m | +14.7% |

Source: Public Accountant; Australian Financial Review

We will now have to wait to see whether this Australian problem is a sign of things to come, or merely a temporary glitch in one market.

Case study: PwC’s betrayal of trust

PwC’s government tax leaks scandal remains perhaps the darkest episode of the Big Four’s recent years. PwC didn’t just neglect a client; it deliberately betrayed an entire state, Australia, as it was trying, sensibly or not, to reduce multinational tax avoidance.

The PwC episode began when senior partner Peter-John Collins signed confidentiality agreements, as part of a project to help the Australian government draft rules aimed at preventing multinational tax avoidance. Collins then shared those secret drafts with colleagues, who in turn sold them to some of the multinationals concerned. The effect was to sabotage the rules before they ever passed into law.

“[That] one is unusual, just in terms of how serious the ramifications were,” says Gow. “It was one of their larger markets, and it had real consequences … They lost a lot of business.” Senior PwC figures did not just breach ethical rules, but also simple good sense, gambling their firm’s entire reputation for a relatively small slice of revenue.

The consulting slowdown may continue

Management consulting and business advice supercharged the Big Four’s growth in the 1990s and then again after 2012, turning them from accounting firms into consulting conglomerates. They made billions implementing cloud computing, enterprise resource planning systems and, more recently, artificial intelligence. And there’s a lot to be made. The global consulting business may be worth as much as US$1 trillion a year – quite possibly 50% more than the accounting and tax advice business. (Estimates appear to be both unclear and unreliable.)

But consulting and advisory is no longer the standout growth market that it was in the 2010s. Big Four revenues for this subsector have slowed since 2022. That is part of a general slowdown that has seen even the prestigious McKinsey consulting firm cut headcount by an estimated 11% between 2022 and the end of 2024.

Source: Big Four annual reports/Wikipedia

It is worth noting that consulting is not responsible for most of the scandals on the list above: the bulk of those come from traditional accounting activities. Even in PwC’s tax leaks scandal, most of the architects were tax experts with legal backgrounds, as Ian Gow acknowledges.

Gow nevertheless argues that consulting work is changing how the firms function. “The culture you have when you’re a firm that’s very involved in advisory is not necessarily the ideal culture you would have for a firm that’s very much into auditing,” Gow notes. “If you’re more entrepreneurial, you’re more chasing revenue… that is not necessarily a good model to be inside the same four walls as auditing”.

Gow and others argue the consulting business is being disrupted by at least three connected forces:

AI tilts the staffing profile

In the popular “pyramid model” of consulting, firms support a small corps of experienced and expensive consultants with an army of cheaper graduates who do much of the research.

But AI tools can now perform some of this research. There’s debate over the effect this will have. But some analysts argue firms need to shift to an “apprenticeship” model or hire more experienced, expensive staff, slicing margins.

Gow agrees new accountants are likely to be supplied by a system that does not rely in university graduates. “The demand for people with almost no skills but a little bit of knowledge is going to go to zero very quickly,” he says.

AI alters capital needs

Gow has long argued that the Big Four’s thin capital bases leave them vulnerable to a need for substantial investment. The AI seems to ask for exactly that: billions to pay for AI platforms, data centres and software licenses. A standard corporation retains much of its yearly profit to re-invest; a partnership generally aims to distribute it to the partners.

“The Big Four model is not that amenable to raising large amounts of capital or making very large capital investments,” he argues. “Technology is just inherently … demanding of capital.”

Private equity enters the market

Private equity firms have aggressively invested in mid-tier accounting and consulting firms such as Grant Thornton and Baker Tilly in the US. They seem to be betting that they can fund the necessary tech upgrades that traditional partnerships may struggle to afford. These groups can tap markets for the necessary cash, while traditional firms must fund investments out of partners’ pockets.

“The culture you have when you’re a firm that’s very involved in advisory is not necessarily the ideal culture… for auditing.”

Ian Gow

Reform freezes on Everest

While scandals like PwC’s tax leaks episode have displayed ethical and competency issues, EY’s Project Everest showed how hard it may be to change the Big Four’s structure. Announced in 2022, Everest aimed to slice EY into two pieces: A regulated, lower-growth audit-oriented firm and a higher-growth, unregulated consulting business. This second business would not only be free to work for audit clients it was previously banned from touching; it could also more easily raise needed external capital. EY estimated this could unlock $10 billion a year in extra revenue.

Gow agrees there was a “very, very strong logic” for this structural split. Regulators wanted splits too: in 2020, the United Kingdom’s Financial Reporting Council actually ordered the Big Four to put their UK auditing and consulting practices in separate business units by 2024. (This was operational rather than full structural splitting, and left the firms still single, integrated legal entities.)

Yet in April 2023, EY’s global structural split plan collapsed. The main reason: partners couldn’t agree on where the tax partners fit. Auditors need tax experts to check the books; consultants need them to sell schemes. Gow says tax emerged as the area where the case for a single firm was “most compelling”. And powerful national EY offices – including the US – rebelled against their global headquarters’ idea, fearing that it would reduce their partner income.

Everest’s failure seems to have ended discussion of structural separation within the firms themselves.

The “Big Four” brand endures

In most industries, different brands manage to set themselves apart through their special approaches, interests and skills.

As Ian Gow points out, the Big Four have largely dispensed with brand differentiation. Instead, they operate as a shared brand, a sort of Big Four Inc. When one firm stumbles, the market simply rotates to the other three. When the PwC tax leak scandal broke, clients didn’t flee to boutique firms; they fled to Deloitte and KPMG.

Indeed, the “Big Four” shared brand appears far more important to clients than any specific firm banner. Corporate boards need a Big Four audit stamp to satisfy investors, and only four stamps are available.

That gives the Big Four a peculiar resilience.

Conclusion: Will the cracks widen?

The Big Four are at an important moment. They have survived scandals that would have destroyed lesser firms. Their revenues are higher than ever. Their ties to the giants of the global economy – and their ability to extract fees – remain strong.

But the cracks are visible. Consulting has made the Big Four rich, but it has also helped to undermine their image of integrity. Audit failures continue. The dissolution of Project Everest suggests the Four are structurally rigid and difficult to reform. And AI may demand capital they don’t have, while undermining their workforce model.

Gow’s final assessment is a mix of scepticism and respect for their survival instincts. He views their greatest potential threat not as regulation – which they always seem to outmanoeuvre – but as technological disruption. “The threat would be that [AI] could be sufficiently disruptive that it requires a different business model… that requires more capital than the Big Four are set up for,” Gow warns.

If a private equity-backed competitor can build a better, cheaper, AI-driven audit machine, the Big Four might finally find that their “shared brand” protection has run out. Continued scandals and more government withdrawals would certainly weaken their position further.

For now, however, they remain the Big Four: battered, conflicted, but with revenues still pouring in.

Explore the IPA’s online CPDs to enhance your skills, from self-managed superannuation funds to tax updates.