At a glance

- Major banks retreated from SME lending after COVID, raising finance barriers for small businesses.

- SMEs now increasingly rely on non-bank lenders, fintechs, and private credit providers for funding.

- Accountants play a crucial role in guiding SMEs through complex, sometimes risky, alternative finance options.

Accountants advising SMEs work in a changing small business lending space. Powerful forces have brought a major shift in funding appetites, particularly amongst the big four banks.

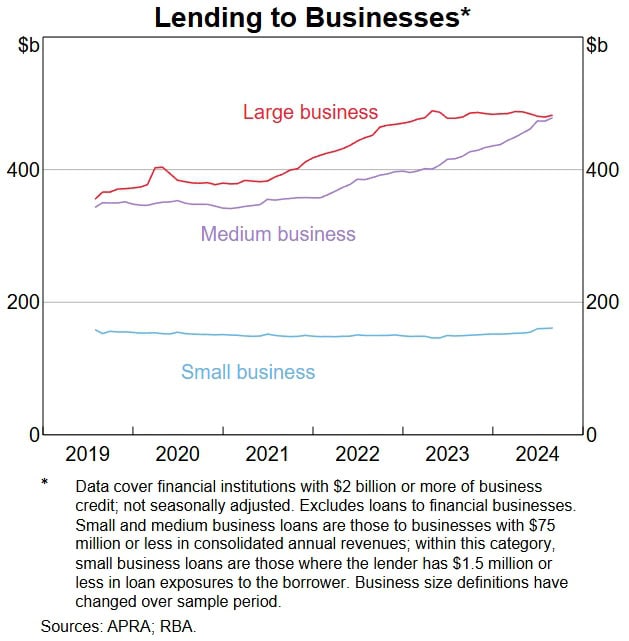

The Reserve Bank of Australia (RBA) set this out plainly in its October 2024 Bulletin. “Increases in the cash rate have led to tighter financial conditions for small businesses,” it said. It added that for many of these businesses, access to finance “remains difficult”. The result? While lending to larger businesses began rising again after the COVID slowdown, small business lending has actually stayed lower than it was before COVID began, at least once inflation is accounted for.

How the capital crunch happened

All is not lost, says Australian Small Business and Family Enterprise Ombudsman (ASBFEO) Bruce Billson. To understand potential solutions, Billson says, it’s first vital to know the background.

“During COVID, the banks undertook a major review of their small business lending books to consider their exposure,” he says. “Even facilities that hadn’t been drawn upon, like unused overdrafts, were cancelled as banks assessed total potential indebtedness. It wasn’t just about active loans, it was about risk buffers.”

At the time, Billson says, it wasn’t unusual for small and family businesses to have a cashflow loan, a working capital loan, various finance arrangements for equipment as well as an overdraft facility that may or may not have been called upon.

“The banks were looking at those things and looking at the total level of potential indebtedness at a time of significant uncertainty,” he says.

“There was an effort by the banks to get alongside their customers and figure out whether the small business financing options were appropriate, reasonable and within their risk appetite. Some were not.”

But as debt was reduced amongst small and family businesses, the solution leaned too far in the opposite direction. SMEs suddenly had nowhere to turn for financing.

In a 2024 report on SME lending, Foresight Analytics argued that “Australian banks have largely retreated from all types of lending bar residential mortgages”.

The problem is now particularly relevant for businesses operating without significant real estate assets. The bank hunger for bricks-and-mortar security has sometimes led to business loans being secured by owners’ homes.

“Finance is the oxygen of enterprise,” Billson says. “If it’s not appropriately available, it will starve off growth and opportunity.”

What are SMEs’ new options?

Billson was a founding director of Judo Bank. “We were set up to take on the big banks because we didn’t think they were being sufficiently responsive to the small business lending appetite,” he says. “There was research at the time showing a very substantial unmet need in the business community.”

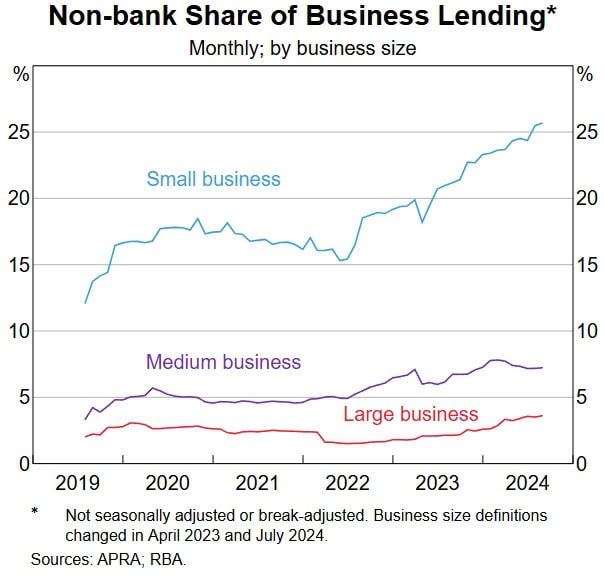

That unmet need seems to have triggered a major change in the makeup of small business lending since 2022. The Reserve Bank’s October Bulletin said its discussions with banks and other finance market players “has suggested some non-banks have competed more aggressively for small and medium-sized business loans”. Some of that change could be due to tougher big bank competition in the mortgage market.

For SMEs, small banks have been an important alternative to the majors. Also important have been non-bank lenders, a group that includes lenders like Firstmac (also operating as loans.com.au), ScotPac, Prospa, Moula, OnDeck, and Capify.

The Reserve Bank says the non-bank lenders are writing the bulk of their business in financing assets such as plant and equipment, rather than property, where the bigger banks have focused. Other options for SMEs include fintechs, private credit providers and revenue-based financial models.

The good news is that the Reserve Bank reported overall lending to SMEs grew by 12% in the year to October 2024.

How can accountants help SMEs?

Billson says disaggregation is the big story, now.

“You haven’t just got a handful of central players any more,” he says. “There are now dozens of lenders. But the downside is that SMEs need help navigating that complexity. That’s where accountants are absolutely essential.”

A survey by RetailBiz in 2023 found 11 per cent of SME respondents “expressed concerns about their existing loan obligations, while a significant 76 per cent of respondents believed that surging interest rates and inflation would have an impact on their cash flow … 30 per cent expected difficulties in collecting customer payments, 26 per cent anticipated struggles in attracting sales, and 20 per cent believed that both factors would affect their cash flow.”

“There are now dozens of lenders. But the downside is that SMEs need help navigating that complexity.”

Bruce Billson, Australian Small Business and Family Enterprise Ombudsman

It adds up to the fact that a large chunk of SMEs have no financial lifeline. Therefore, the quality of finance they receive is vital to their survival.

Many fintechs and non-bank lenders are responsive and well regulated, Billson says, but others exploit desperation.

“Some have punishingly high interest rates and frankly, some of them have unconscionable penalty regimes if you miss a payment,” he says. “If they’re not a member of AFCA, my advice is simple – no, thank you.”

Accountants are uniquely placed to help clients avoid these pitfalls, Billson says. Their role is not just connected to tax compliance, but is also about financial literacy, planning and helping clients become finance-ready. He runs through the questions they can help answer:

“What reasonable steps should a business owner take to put themselves in the best possible position to explain to a potential financier what it is they’re looking for, how it fits within the business picture in terms of what they might do with those funds, and what’s the assurance around the likelihood of repayment?”

“Know your numbers, be able to explain them and have a clear plan for how the funds will be used. These are not just good habits, they’re essential to securing the best finance terms.”