Treasurer Jim Chalmers handed down his third budget, forecasting a second surplus of $9.3 billion in 2023-24 followed by a sea of red tape over the next four years. There are bold expectations that the level of inflation will be back in the Reserve Bank of Australia’s target band sooner than expected.

The Institute of Public Accountants believes the budget did not go far enough to address Australia’s complex taxation system to boost productivity, competition and innovation for small businesses.

IPA’s General Manager Technical Policy Tony Greco examines the Treasurer’s announcements, budget inclusions and the bottom line for tax, accounting and small business.

Little relief for small business

The budget centrepiece, Future Made in Australia, does not appear to have any focus on small and medium sized businesses (SMEs). Many are grappling with the increasing cost of doing business and face being left behind.

The Australian Small Business and Family Enterprise Ombudsman estimates that 43 per cent of small businesses are currently not making a profit, with 75 per cent taking home less than the average wage despite working longer hours than average employees.

Sustained cost of living pressures have eroded consumer spending and demand for goods and services, which has hurt the small business sector and consumer confidence more broadly.

Small business instant asset write-off

The small businesses instant asset write-off will be extended for another year until 30 June 2025. Businesses with a turnover of $10 million or less will be able to deduct $20,000 from eligible assets.

While this is a welcome measure, it is not a permanent feature of our tax system and subjected to the whim of the government each year. Small businesses may not want to invest in ageing capital assets until their profitability improves.

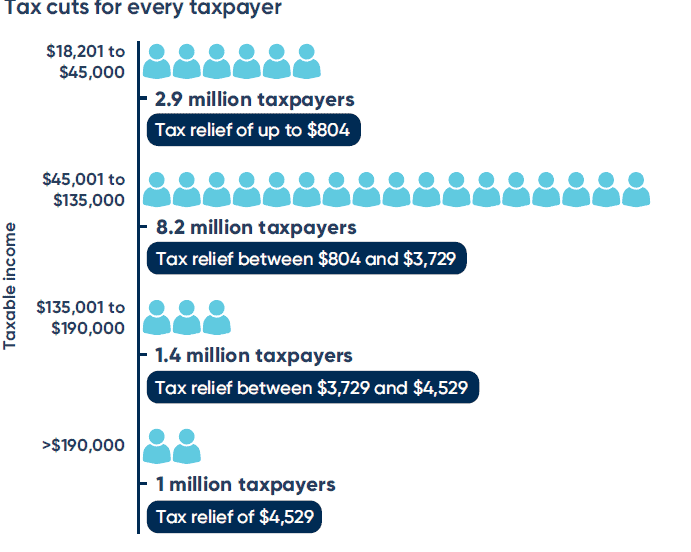

Stage three tax cuts

Some 70% of small businesses that are unincorporated owners will benefit indirectly from the stage three tax cuts.

Under the tax cuts in 2024-25:

- The 19% tax rate will be reduced to 16%.

- The 32.5% tax rate will be reduced to 30%.

- The income threshold at which the 37% tax rate applies increases from $120,000 to $135,000.

- The income threshold at which the 45% tax rate applies increases from $180,000 to $190,000.

Modest small business measures

The government will also provide $41.7 million over four years from 2024–25 to support small businesses with regulatory and support services.

This includes:

- $25.3 million to support the Payment Times Reporting Regulator to implement reforms recommended by the statutory review of the Payment Times Reporting Act 2020.

- $10.8 million over two years from 2024–25 to extend the Small Business Debt Helpline and the NewAccess for Small Business Owners program to continue to provide financial counselling and mental health support for small business owners.

- $3 million over two years from 2024–25 to implement the government’s response to the Review of the Franchising Code of Conduct. It will investigate the feasibility of a licensing model and remaking and updating the Franchising Code of Conduct before it expires in April 2025.

- $2.6 million over four years from 2024–25 (and $0.7 million per year ongoing) for the Australian Small Business and Family Enterprise Ombudsman to support unrepresented small businesses to navigate business-to-business disputes through alternative dispute resolution.

Import tariffs removed

Some 457 nuisance tariffs will be removed from 1 July 2024 streaming the importation of $8.5 billion worth of goods annually (toothbrushes, hand tools, fridges, dishwashers, clothing and menstrual and sanitary products).

Debts on hold

The Commissioner of Taxation will be given the discretion to not use a taxpayer’s refund to offset old tax debts, where the Commissioner had put that old tax debt on hold prior to 1 January 2017. This discretion will apply to individuals, small businesses and not-for-profits and will maintain the Commissioner’s current administrative approach.

ATO fraud crackdown

The government will spend $187 million over four years from 1 July 2024 to strengthen the Australian Taxation Office’s (ATO) ability to detect, prevent and mitigate fraud against the tax and superannuation systems. This includes:

- $78.7 million for upgrades to information and communications technologies to enable the ATO to identify and block suspicious activity in real time.

- $83.5 million for a new compliance taskforce to recover lost revenue and intervene when attempts to obtain fraudulent refunds are made.

- $24.8 million to improve the ATO’s management and governance of its counter-fraud activities, including improving how the ATO assists individuals harmed by fraud.

The Government will extend the time the ATO has to notify a taxpayer if it intends to retain a business activity statement (BAS) refund for further investigation.

The ATO’s mandatory notification period for BAS refund retention will be increased from 14 days to 30 days to align with time limits for non-BAS refunds. Any legitimate refunds retained for over 14 days would result in the ATO paying interest to the taxpayer (as is currently the case).

This will have effect from the start of the first financial year after the legislation takes effect.

Anti-money laundering and counter terrorism reform

The Government will provide $168 million over four years from 2024–25 to implement reforms to strengthen Australia’s Anti-Money Laundering and Counter-Terrorism Financing Act 2006, to enhance Australia’s ability to detect and disrupt illicit financing.

Funding includes:

- $160.8 million over two years from 2024–25 for the Australian Transaction Reports and Analysis Centre to expand its regulatory, intelligence and data capabilities and provide guidance to newly regulated entities.

- $7 million over four years from 2024–25 for the Attorney-General’s Department to support the implementation of the legislative reforms through the provision of policy and legal advice and stakeholder consultation. It will also deliver a program of anti-money laundering and counter-terrorism financing capacity building in the Pacific.

- Funding from 2025–26 for this measure will be held in the Contingency Reserve until the legislative reforms have passed the Parliament.

Securing a better future for small business

There was not a lot of joy for small businesses facing significant headwinds. Like individuals, SMEs are also suffering from the cost of doing business crisis, with eroding margins eating into profitability.

Small businesses are looking for any red tape reduction and productivity boosting incentives to help absorb cost pressures that are threatening their financial sustainability.